Could you cope with over half your take-home pay spent on your mortgage? The Bank of England thinks so.

Published: by Adam van Lohuizen

The Bank of England (BoE) on Monday released its quarterly bulletin, which amongst many other things, looked at the impact of higher interest rates on the household sector. The main finding reported from the survey was that most households could handle a 2% increase in interest rates.

But what does this actually mean? The BoE says households can handle their mortgage when they don’t need to spend more than 40% of their pre-tax income on paying it off. It used this measure because after this point there is a big jump in households entering arrears on their mortgages. But just because households are able to ‘handle’ rate increases without immediately going into arrears, it doesn’t mean they can afford them.

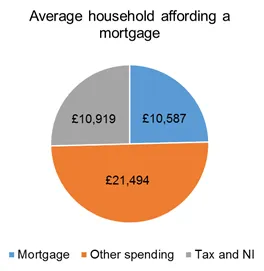

Forty per cent of pre-tax income equates to a staggering 54% of income after tax for the average household on a single income. So over half of your take-home pay is spent on your mortgage before the BoE thinks you’re at risk. This is a far higher threshold than one-third of disposable income – the broadly accepted benchmark of affordable housing costs.

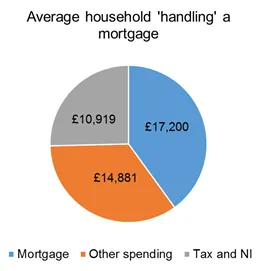

Comparing the difference between the household budgets between these two measures demonstrates how big the gap really is. The average income for a household with a mortgage is £43,000 per year according to the survey. For a household with a sole income, an affordable mortgage would leave over £21,000 for spending on living expenses, but the BoE believes that this household can get by on under £15,000 per year, almost a third less to spend on food, utilities, clothing and all other living expenses.

No wonder the survey found worry and concern amongst mortgage holders. Almost half of households with mortgages said they were concerned about their mortgage debt, and a quarter of households have already cut spending because of these concerns. There is even some evidence that suggests some households which are more at risk have already cut spending as much as they can, making them even more vulnerable to higher interest rates.

The BoE then tested a scenario in which interest rates go up by 2%, and household incomes increase by 10%, to see how this would affect mortgage holders. It found that the percentage of total households who couldn’t handle their mortgage would increase from 1.3% to 1.8%. This doesn’t sound like much, but this is actually an increase from around one in every 73 households to around one in every 55, or an increase from around 360,000 to 480,000. An additional 120,000 families struggling to make ends meet doesn’t seem so small now.

These impacts will be even more severe if incomes don’t increase by 10% to match the rise in interest rates. Given it has taken more than six years for average nominal incomes to increase by 10% (a period where real incomes have fallen), there is every chance that the assumed income growth won’t meet the 2% in rate rises expected over the next three years or so.

The findings of the survey focus on the impacts and risks financial stability arising from increases in interest rates, because that’s the job of the BoE: to maintain financial stability.

But the results also tell us much more. They demonstrate the dire state of housing affordability. They show that households are already struggling with their mortgages, and that they will find it even harder when interest rates rise.

When rates eventually do start to go up, it will be vital that everyone – households, banks, advice providers like Shelter, and the government – is properly prepared.