Help to Buy Equity – a welcome addition?

Published: by Sara Mahmoud

Last week, the government published a report on the impact of the Help to Buy Equity scheme. Launched in April 2013, it provides buyers of new-build properties registered with the scheme with an equity loan worth 20% of the value of the home. Alongside the report, a rather sweeping press release proclaimed ‘43% additional new homes built as a direct result of Help to Buy equity’. With an extended policy recently launched in London, does this prove that Help to Buy is a valid solution to our affordability crisis?

Extending credit, boosting supply?

Both the Help to Buy Equity and Mortgage Guarantee schemes aim to open up credit to first-time buyers with small deposits, following the post-Financial Crisis contraction in high loan-to-value lending. The explicit tying of the Equity scheme to new build properties means its other important aim is to stimulate house building.

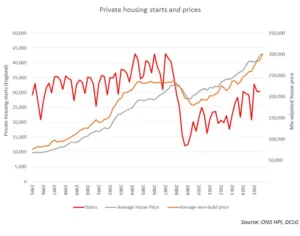

Most people can’t afford to buy a home outright, so demand for housing is based not only on incomes but on how easy it is for people to borrow. As a result, the sharp contraction in lending caused by the Financial Crisis contributed to a 14% fall in house prices. In turn, the drop in prices that developers could fetch for their properties led to a whopping 71% drop in starts between 2007 and 2009.

Help to Buy works on the assumption that housing supply is ‘demand led’; developers only build what they can sell, so stimulating demand by boosting how much buyers can borrow ought to boost supply. The government evaluation therefore assumes that any additional homes bought through Help to Buy resulted in at least one additional new home built.

This idea of additionality is central to assessing whether the policy has worked at boosting house building: if people who could have bought anyway used the scheme, then it simply meant more money chasing the same number of homes. The only effect would be to push up prices.

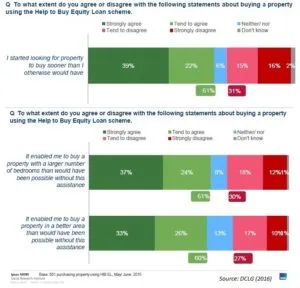

To quantify this, researchers surveyed a sample of buyers who had used the scheme. They found that 43% would not have been able to buy the property they moved in to or something similar second-hand, without the support from Help to Buy. Given that 33% of new build sales were funded using Help to Buy this implies 14% of them would not have happened without the scheme. They assume this led to 14% of new build starts since the policy launched.

A leg up to the credit-constrained?

There are legitimate technical concerns over how this number was calculated, but even if we take the government figures at face value, they imply that over half of those surveyed could have bought a similar home anyway. In fact, 9% could have afforded the home they bought without Help to Buy at all.

Buyers who really were additional were older and more likely to have purchased a detached house. The first time-buyers who were additional had similar incomes to first-time buyers nationally, suggesting the only difference Help to Buy made was that some of them didn’t need to wait as long to save for a deposit.

Putting this all together, although the scheme genuinely helped some people on middling incomes buy bigger new builds in nicer areas sooner, over half of those using the scheme didn’t really need it. This implies that a large chunk of Help to Buy Equity sales could at best be a waste of public money and at worst, an inflationary boost to house prices.

A boost to building?

When it comes to the impact on supply, there is also the question of the counterfactual – or what would have happened without Help to Buy Equity. The report acknowledges that it is hard to disentangle its effects from the wider context – not least the Mortgage Guarantee scheme, introduced six months beforehand.

It also points to evidence that, by the time Help to Buy Equity was introduced, house prices and buyer confidence were increasing and the plummet in starts had already reversed. None of the developers interviewed for the evaluation ‘mentioned any slow-down in sales’ before the policy was implemented and although the larger developers said that it led to an increase in output, there is very little evidence for this in official figures on building.

All in all, it isn’t clear that Help to Buy Equity has achieved its stated goals. My next blog will examine whether the policy of boosting supply by supporting new build demand makes sense, particularly in London.