The Housing and Planning Bill risks missing out half of England’s young private-renting households

Published: by Sara Mahmoud

This afternoon, the House of Lords will kick-off the first round of voting on key amendments to the Housing and Planning Bill. Councils around the country will be forced to make sure that 20% of all new homes on developments are Starter Homes, leaving very little room for social rent. Given that the government’s vision for affordable housing is almost exclusively through subsidised home ownership, it’s crucial to ask whether this does the job, particularly for households on lower incomes.

We’ve long warned that Starter Homes will be unaffordable to families on typical incomes. Our new figures go further and suggest that relying on Starter Homes, Help to Buy and shared ownership risks leaving behind at least half of all young private-renting households in England.

What does low and middle income mean?

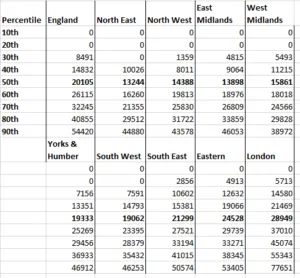

If a policy is to meet the needs of priced-out low and middle income households, we need to understand how much these households really earn. Levels of employment vary around the country and the rise of zero-hours contracts means that understanding how much actual low-paid households earn means using the Family Resources Survey.

The table below gives post-tax earned income deciles for private renting households under 40 in each region. Crucially, this is the money in actual households’ pockets that is not related to benefits.

Source: Family Resource Survey

How much do you need for a home?

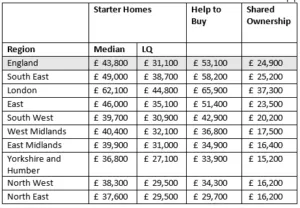

The next step is to estimate how much households will need to earn to access the different housing offers. Following the same methodology in our London-focused analysis , we calculated the minimum household annual income needed.

This analysis uses average house prices to estimate what each offer is likely to cost, average advances and loan to income ratios for first time buyers and took in to account typical rent and service charges for shared ownership. Of course, how much Starter Homes will cost is highly uncertain, so to give the government the benefit of the doubt we calculate what a household needs to purchase a cheap, lower-quartile new build as well as a more typical median one.

Sources: ONS HPI, HPSSA, CML, NAO

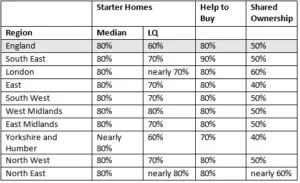

How many households left behind?

The proportion of young renting households missed out is then given by comparing the two tables.

Even assuming the cheapest potential price for Starter Homes, 60% of young renting households in England will be excluded from them. DCLG have pointed to the average price for first-time buyers excluding London of £181,000 as indicative of what Starter Homes might cost before the discount. To afford this, a household would need an income of £34,000. The median post-tax earned income for renting households under 40 outside of London is just £19,000 – so the government’s own figures suggest Starter Homes will only be available to the top 30% in the rest of England.

Worryingly, house prices are so high that even shared ownership is out of reach for half of young private-renting households in England. If you’re used to healthy take home pay the income needed to afford shared ownership, around £25,000, could look easy to achieve. The median amount that real renting households under 40 actually earn, however, is around £5,000 less than this.

Source: Shelter calculations

We need genuinely affordable, rented housing too

This research clearly shows that when actual households are considered, the solution to the housing crisis offered in the Housing and Planning Bill doesn’t add up. Forcing local authorities to provide unaffordable Starter Homes and channelling all government investment in to them and shared ownership risks leaving a sizeable chunk of young households behind in the unstable and expensive private rented sector.

This has consequences for our housing benefit bill, as well as for the families trapped in housing insecurity. Let’s hope that the Lords vote to do the right thing this afternoon and that the government is willing to listen.