Lies, damn lies and rent statistics

Published: by John Bibby

Here’s a quick quiz: how much are rents going up by in England?

A) 7.5%

B) 1.4%

C) 4.6%

D) 1%

E) They’re not rising, they’re falling

It’s a tough one, but if you answered any of A, B, C, D or E then congratulations! You can make a case for being right. All five are estimates of the increasing cost of renting that have been published in the last month.

But there’s a problem, surely: they can’t all be right. So why the wide disparity between the different results?

Part of the answer simply lies in which data the measures are based on.

The first three measures are all made by private property companies based on their own business data (A is from tenant referencing and insurance company HomeLet, B from estate agent group LSL and C from estate agent group Countrywide). All are thus based on different datasets and the differences between their results likely accounted for by differences in the geographic distribution or market focus of their clients.

In a sense this means they can also all be right: the amount that HomeLet’s clients are charging in rents can go up by 7.5% in the same year that LSL and Countrywide’s increase more slowly. They just don’t all accurately reflect the rate of change in market rent for the whole country. And the likelihood is that none of them reliably, consistently and accurately do it.

Which brings us to D and E, the government’s stats: from the ONS’s Index of Private Housing Rental Prices (referred to as the ONS stats throughout the rest of this post) and DCLG’s English Housing Survey respectively. These are both also based on different datasets – the ONS stats are based on a matched sample from Valuation Office Agency data and the English Housing Survey on its own survey sample of 2,500 renters.

But the differences don’t stop there. It is not just that the government stats are based on a different – presumably more balanced – sample and are therefore more right than the private estimates. Both sets of government stats also aim to measure something different from the private property companies’.

The private company stats purport to measure changes in market rents: the amount of rent that landlords charge new tenants (whether advertised or achieved). By contrast, the ONS stats and English Housing Survey try to measure uplift in the amount that all renters actually pay, including both new tenants and those already in rented accommodation.

To illustrate the difference, let’s consider a comparison. The private companies’ rent indexes are similar to familiar measures of house price inflation (such as those published by Nationwide or Halifax every month). Just as the house price figures measure how much prices of houses sold in the last month have gone up since this time last year, the rent figures measure how much rents have gone up for new tenancies last month compared to a year ago. In contrast, the government stats are more like the owner-occupier housing elements of RPI inflation (interest rate payments and property depreciation) as they mix in the costs incurred by people who have just bought a house with those who have been in their home for years or even paid off their mortgage.

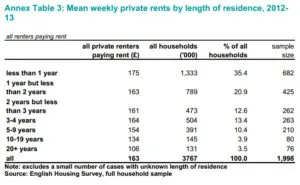

It is a critical difference, because those paying the lowest housing costs and facing the smallest increases – both for private renters and owner occupiers – are those who have been in their homes for the longest length of time (as demonstrated in the table from the English Housing Survey below).

It’s reasonable to expect, therefore, that increases in both the ONS and English Housing Survey stats will be smaller (and less volatile) than actual increases in market rents.

This is not to say that the government statistics are not useful – and it’s certainly an improvement on a few years ago when the ONS published no rent statistics at all. Policymakers should be able to refer to a measure of the cost of renting for all renters, to inform decisions affecting the whole of the private rented sector, rather than just new renters.

But they also need clear information on how rents that are available on the market are changing – and this is the missing piece of the jigsaw.

When we talk about increases in house prices we typically think in terms of the amount that I would expect to pay if I bought a home today. We don’t include in the equation historic prices paid by people who bought ten or twenty years ago. Because of this cultural association, there is a danger that when the ONS stat is used in policy discussions to talk about increases in rent, what it actually measures is misunderstood.

And it’s important to know what you’re talking about when you’re discussing rent measures – not least as politicians have been known to trade blows about whether rents are actually rising or not.

As the ONS stat will under-report recent changes in rents, the danger is that policymakers won’t be able to spot spikes in market rents. After all, why would you worry when the official rent statistics suggest rent increases are so low?

What this misses is that, unlike owner-occupiers, private renters move frequently. Each year, a quarter of private renters will move and start paying a new market rent – and so market rents have a big impact on their housing costs.

This is why Shelter recommends that the government commission ONS to start tracking market rents. We fed this into ONS’s consultation on the Index of Private Housing Rental Prices earlier this year and they are now considering this.

Of course, even with entirely robust and comprehensive statistics, renters will still be subject to the possibility of sky-high market rents, unless we get a better deal for renters. But accurate and well-understood statistics can help to make the case for change.