Static models cannot explain the failings of a dynamic housing market

Published: by Toby Lloyd

In this guest Blog, Thomas Aubrey of the Centre for Progressive Capitalism takes issue with economic analysis being used to justify slow build out of housing developments with planning permission.

Economists and financial analysts have often struggled to model complex, dynamic systems such as the economy, but since the financial crisis there is an increasing acceptance of the limits of simple economic models. So, I was surprised to read a recent report by the planning consultancy NLP which used a simple static model to explain why there is no incentive for housebuilders to hold on to land to increase profitability.

Their argument is as follows: “When a housebuilder buys land, it increases their total asset value; all things being equal, if this land (or the properties built on it) are not sold, this will decrease its Return on Capital Employed. A reduction in its ROCE may affect how investors view the house builder’s long-term profitability, so the housebuilder is incentivised to maintain (or improve) its ROCE.” The ROCE is a key measure of business profitability that housebuilders target

This model appears to be an attempt to rebut the Secretary of State’s recent criticisms of firms slowing build-out rates, by using the counter-argument that “housebuilders are already incentivised to increase their earnings i.e. build and sell homes as quickly as possible.” With the much-anticipated White Paper tipped to include measures to drive up build-out rates, it’s not hard to guess why some in the industry are keen to make this argument now.

It is indeed true that at any point in time if total assets rise and everything else stays the same then the return on capital employed will fall. The problem is we don’t live in a static world. Time is a rather important factor, and is central to the valuation of companies. To demonstrate this, let’s assume we decide to make our world marginally more complex with a two-year model. In year 1 land values rise and the firm decides not to use its land, so its ROCE falls. However, in year 2 the firm does decide to build and sell houses – so its earnings will increase and its total assets fall (because it no longer owns the land or homes), leading to a much larger increase in ROCE. What matters in the real world is the rate of change of returns through time – not just in year 1.

The challenge for housebuilders is that they need to manage their business across the credit cycle. In these volatile conditions, altering build-out rates depending on what the market is doing is just sensible risk management. In the event of falling land prices it makes no sense to build out at capacity. And during periods of rising land prices, maximising build out rates might leave the firm overly exposed should the market turn. Firms therefore need to try and manage their ROCE through time.

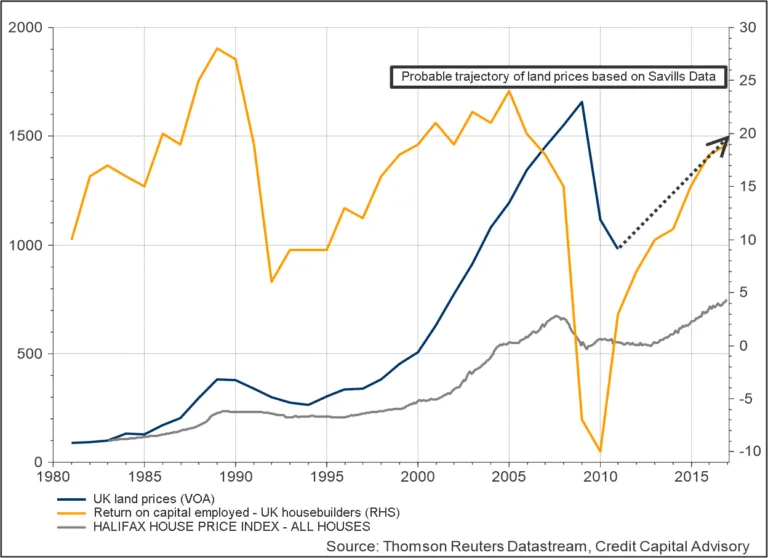

But as the chart demonstrates, managing these risks is very challenging, which is why housebuilders’ share prices are far more volatile than the broader stock market. The average return on capital employed for UK housebuilders is unsurprisingly highly correlated to rising land and house prices. Rising prices drives up ROCE and falling prices drive it down. When these turning points happen is of course unknown – so it is therefore critical for developers to limit their exposure to these risks.

Return on capital employed UK housebuilders, house & residential land prices

Note: As the VOA stopped collecting land data in 2011, the Savills data was used to generate a proxy which suggests that land prices have risen about 50% from 2011.

In addition to the question of developers’ build-out rates, the government is rumoured to be considering measures to reform the land market. On this issue, the NLP report is right that perhaps too much of the debate focuses on housebuilders and not enough on the role the land promoters.

However, the report attempts to justify the role of these intermediaries on the grounds that the land market is opaque and hugely inefficient. This is a timely reminder of just how broken the housing market in the UK is, but NLP seem to be suggesting that any attempt to make this market more efficient would inevitably lead to a fall in housebuilding. Housebuilding rates in continental European have consistently been higher than in the UK since the mid-1970s, largely due to their more efficient land markets. So the idea that housebuilding would fall in the event of a more efficient land market is clearly without foundation.

It is a shame that NLP decided to go to such lengths to defend the dysfunctional aspects of our housebuilding system – especially as the main conclusion of the report is sound: that we need more planning permissions. But for this to happen, Britain needs to step up its infrastructure investment to connect available land to jobs. The problem for the UK is that instead of using land value capture to finance projects as most European and Asian countries do, we have decided that landowners should receive windfall profits instead; a process that Adam Smith argued was a major obstacle to capital accumulation. The Centre for Progressive Capitalism has set out how this could be done with a simple change to the law. The Secretary of State should follow his pro-market instincts and ensure that one of the last bastions of inefficiency and rent extraction finally comes to an end.

Thomas Aubrey

Director, Centre for Progressive Capitalism & Founder, Credit Capital Advisory